The Loonie Hour #77

The Loonie Hour #77

In this week's episode, we dive into the Canadian Federal budget, foreign buyer rules, global macro sentiment, and the Fed's discount window.

The Federal government released its 2023 budget. To absolutely no one's surprises, it outlined more spending and higher taxes. It is a budget that could put government finances on an unsustainable path in the event of a significant economic slowdown. Furthermore, given Canada's record population growth, it included some initiatives at odds with the Bank of Canada's (BoC) attempt to bring down inflationary pressures.

The budget expects a deficit of $43 billion for 2022-23 and forecasts deficits of $40.1 billion for 2023-24, and $35 billion for 2024-25. One major focus of this year's budget is developing Canada's green economy by introducing a slate of corporate tax credits meant to encourage investment in clean energy. Note that Canada is one of the world's more important producers and exporters of fossil fuels.

One fascinating wrinkle is the admission that Canadians will NOT be better off over the duration of their forecast. Usually, even the most sensible government budgets have an optimistic bent. Yet based on the current budget, the average private sector forecasts for GDP growth of 2.0% and for population growth 2.0% (both from 2022 to 2027); Canadians are expected to be no better off in 4 years despite much higher taxes and massive increases in supposed investments.

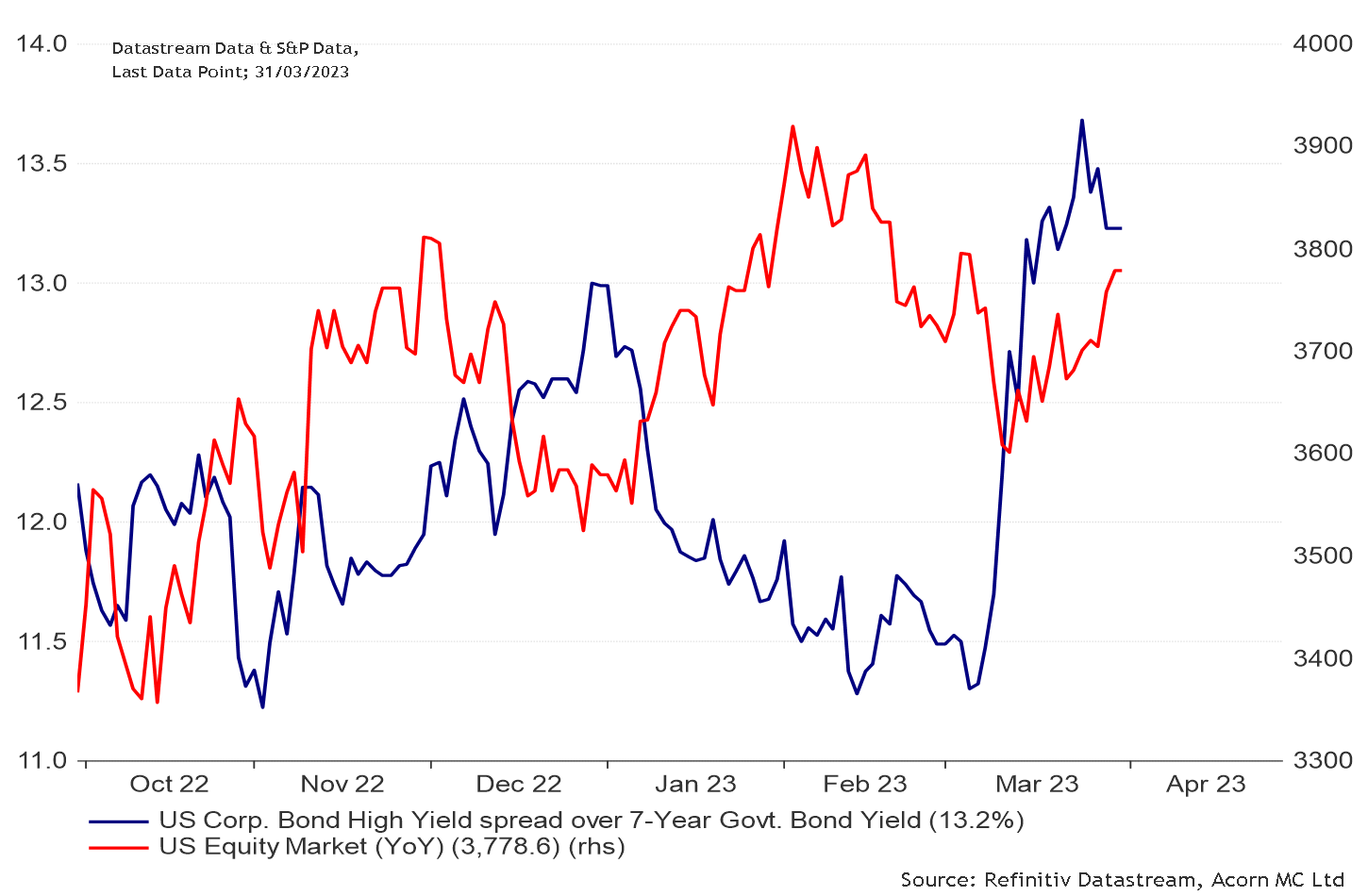

Credit spreads measure the difference between the yield of a risk-free security, such as a Treasury bond and the yield of a corporate bond with a similar maturity. The greater the spread, the higher the perceived risk of the (corporate or government) bond. Therefore, credit spreads provide investors with an indication of the level of risk associated with a particular bond in the credit markets. Credit spreads can also help assess broader market risk. Normally, there is a tight negative correlation between equity markets and credit spreads; when the market rallies, credit spreads contract (go down). The recent rally in equities gives us pause because there has not been a corresponding tightness (contraction) in credit spreads. A worrying sign that the rally in equities may be unsustainable.

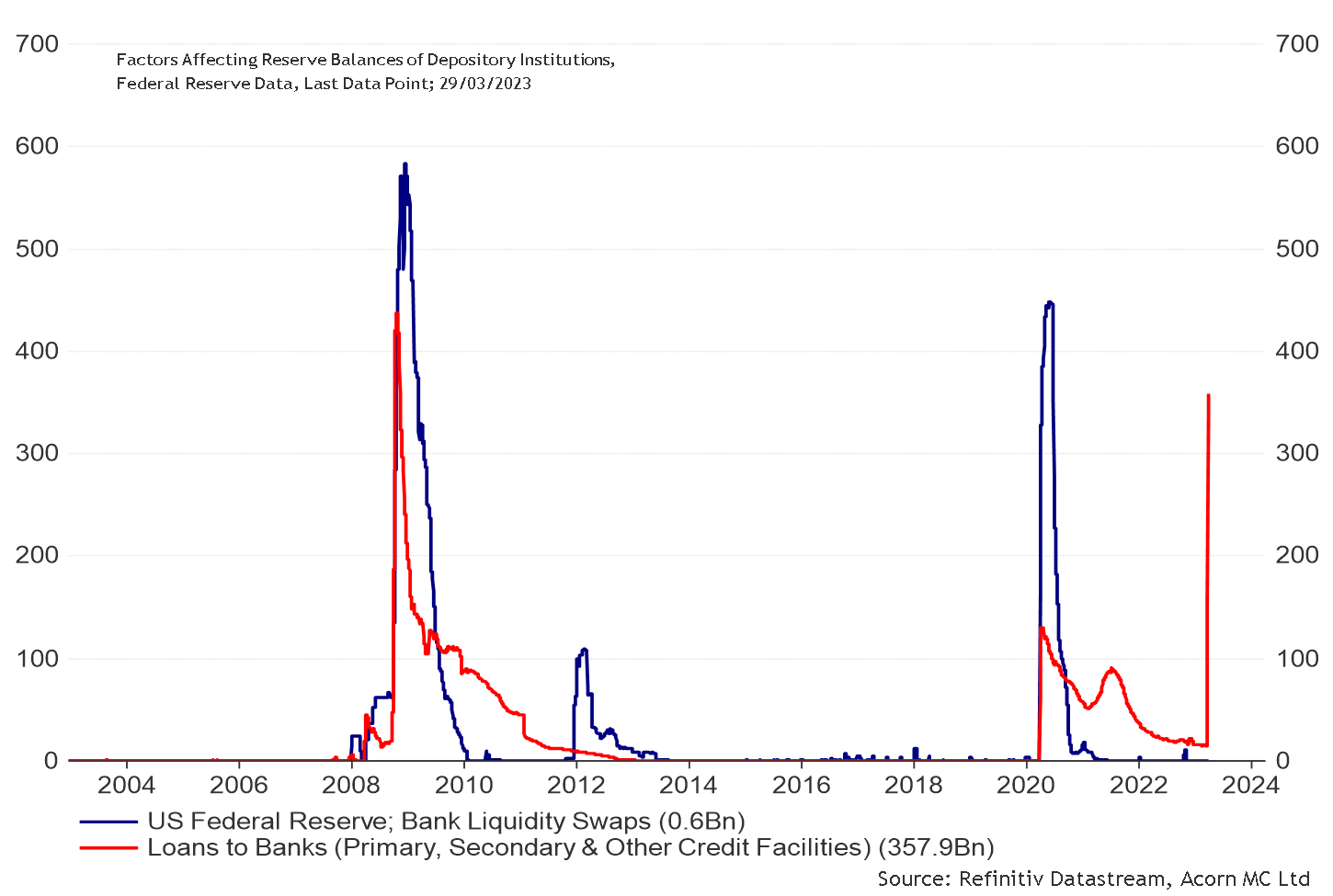

One of the most important roles of the US Federal Reserve is to help relieve liquidity strains for individual depository institutions (banks) by providing a source of funding through the Discount Window. All discount window loans must be fully collateralized, with an appropriate haircut (a discount applied to the value of an asset) applied to the collateral. By providing access to funding, the discount window helps banks manage their liquidity risks efficiently and avoid actions like bank runs that might negatively affect the banking system (i.e., contagion), customers and clients. Thus, the discount window supports the smooth flow of credit to households and businesses.

As the spikes in the chart below highlight, banks draw on the credit facility in periods of stress to meet acute liquidity needs. Once the situation returns to normal, the credit facility can lay dormant for years.

Click below to listen to this week’s episode!