The Loonie Hour #79

The Loonie Hour #79

In this week's episode, we discuss the BOC presser, inflation above and below the boarder, US recession indicators, Buffet in Japan & Germany's asinine energy policy.

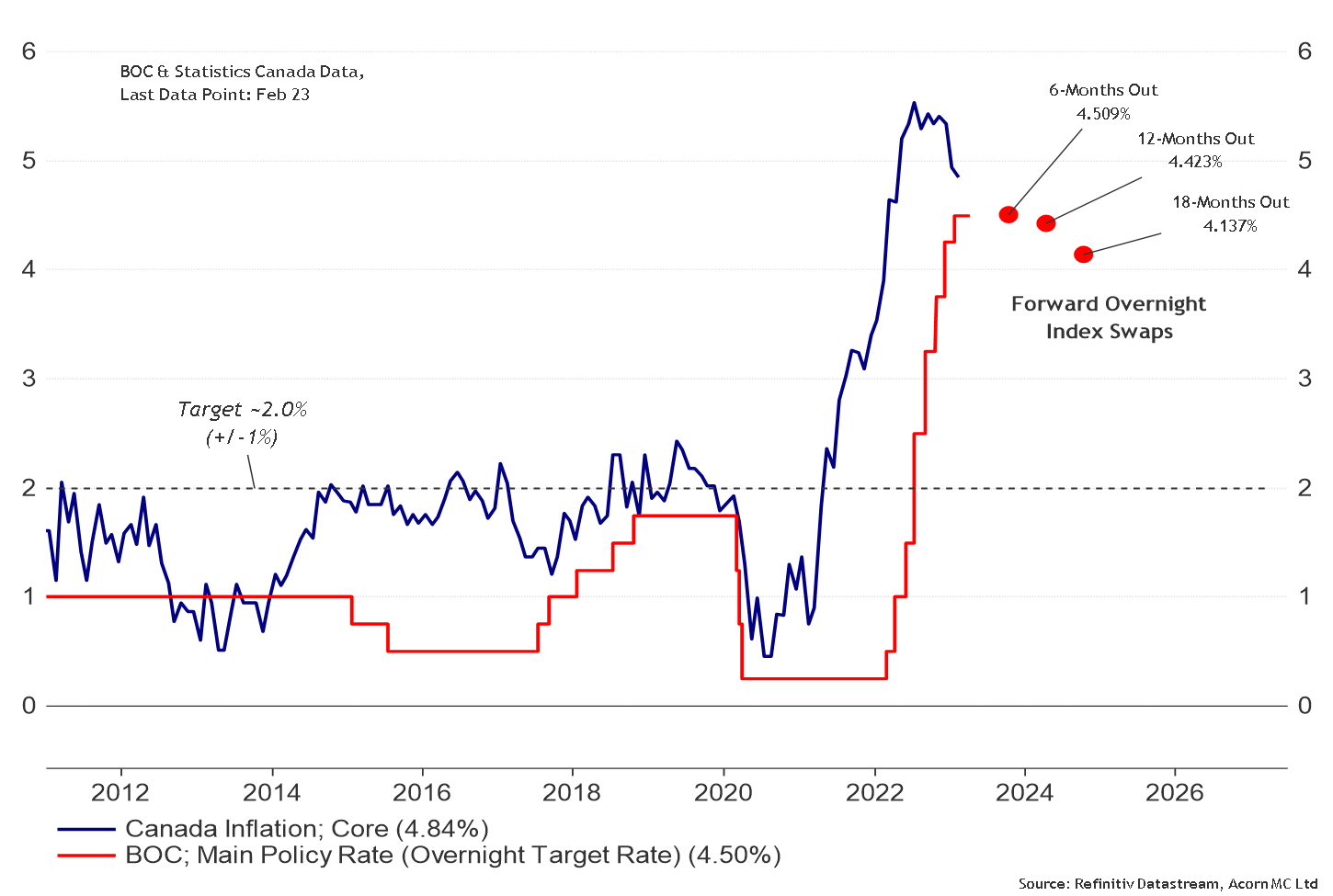

The Bank of Canada (BOC) maintained the policy rate (overnight target rate) at 4.5% and will continue with its quantitative tightening policy. And according to the BOC Monetary Policy Report, “inflation […] should come down quickly to around 3% in the middle of this year because of lower energy prices, improved supply chains and restrictive monetary policy. The Bank projects that inflation will reach the 2% target by the end of 2024.” However, given record immigration, deficit spending, and sticky Services and Shelter components, skepticism remains.

The Governor stated that the Canadian economy is still experiencing excess demand, with a low unemployment rate of 5%, but recent stress in the global banking sector has led to tighter credit conditions, resulting in weaker global growth. The BOC expects weak Canadian GDP growth for the rest of this year, gradually picking up in 2024 and 2025. The biggest upside risk is the possibility of services inflation due to a tight labor market and companies continuing to pass on higher costs without restraint. This could require a longer restrictive policy rate period to reach the target level.

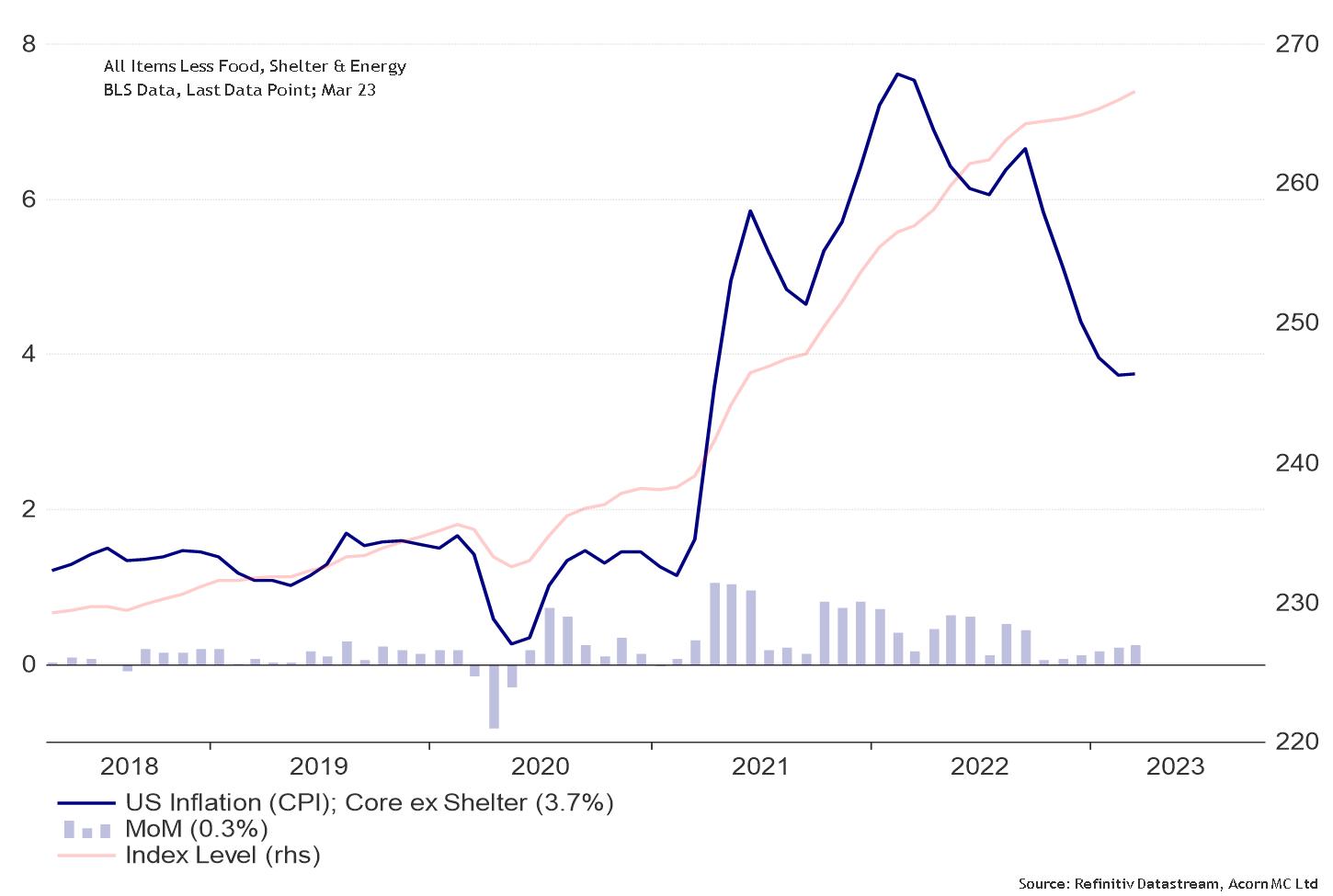

In the US, the Headline Inflation (CPI) data has been released. As with most developed markets, inflation has already peaked and is heading lower. The main consumption basket fell more than expected year-on-year (YoY) to 5.0% (compared to the expected 5.2%) from 6.0% in December. While a drop of 1% is not unheard of, and it has happened six times in the last 40 years, it is a significant monthly decline for a YoY series.

The index for Shelter was the main contributor to the monthly increase, outweighing the decline in Energy, according to the Core Consumer Price Index (CPI) data release. Shelter, which has the largest weight in the Core CPI basket (about 43%), is still increasing and has not yet reached its peak. While some have pushed back on the emphasis on the Shelter component, the argument may become irrelevant as the index for Core CPI excluding Shelter may rise again.

During the podcast, the topic of a potential recession was also discussed, with particular emphasis placed on the strong signal emanating from the yield curve and the New York Fed's recession indicator, which reached a 40-year high. The yield curve, specifically the differential between the ten-year Treasury note and the three-month Treasury bill, represents a valuable forecasting tool due to its consistent outperformance of other financial and macroeconomic indicators in predicting recessions within the range of two to six quarters ahead. The inversion of the yield curve has proven to be a reliable predictor of recessions because it reflects market expectations of future economic conditions. Typically, long-term interest rates are higher than short-term rates to account for the greater risk of lending money over a longer period. However, an inverted yield curve arises when short-term rates are higher than long-term rates, indicating that investors expect weaker economic conditions in the future and lower demand for borrowing in the long-term. This lower demand is indicative of an economic slowdown or recession. Furthermore, the inverted yield curve serves as an indicator that the central bank may need to lower short-term interest rates to spur economic growth, which is another reason why it is a robust predictor of recessions.

Meanwhile in Germany, stupidity has taken hold. In a decisions that should be mocked, derided and shamed for Germany is going forward with plans to shut down the last three remaining nuclear powerplants which, by the way, remain in perfect working order.

At its peak, nuclear power accounted for more than 30% of total electricity production in Germany. However, in 2011, Chancellor Angela Merkel, who holds a PhD in Physical Chemistry, used the Fukushima nuclear disaster to gain political support from the Green party ahead of a state election. Merkel had previously enacted the extension of the nuclear reactors only a few months prior to the disaster.

Merkel cited the Fukushima incident as evidence that the German nuclear plants had become too risky. However, the root cause of the Fukushima disaster was not the earthquake or tsunami, but rather the mismanagement of the plant. For instance, the emergency diesel generators were placed at the lowest point of the sea-facing section of the plant, and the mobile backup generators were located in the basement of the plant's operator's headquarters, 250km away.

While German nuclear power plants had an excellent reputation for productivity with minimal downtime, the Japanese nuclear industry was known for corruption, secrecy, and sloppy maintenance practices for years prior to the Fukushima disaster.

The decision to close the nuclear power plants has been met with criticism, with many calling it reckless, cowardly, and insane. Keeping the plants running for another 5-10 years would have been inexpensive, low-risk, and provided a much-needed source of clean energy. Instead, the country may need to rely more heavily on coal to meet its energy demands, as suggested by Ottmar Edenhofer, the director of the Potsdam Institute for Climate Impact Research.

Click below to listen to this week’s episode!