The Loonie Hour #84

The Loonie Hour #84

On this week's podcast, we discuss Canada's housing market, a possible inflation head fake, and federal government debt issuance.

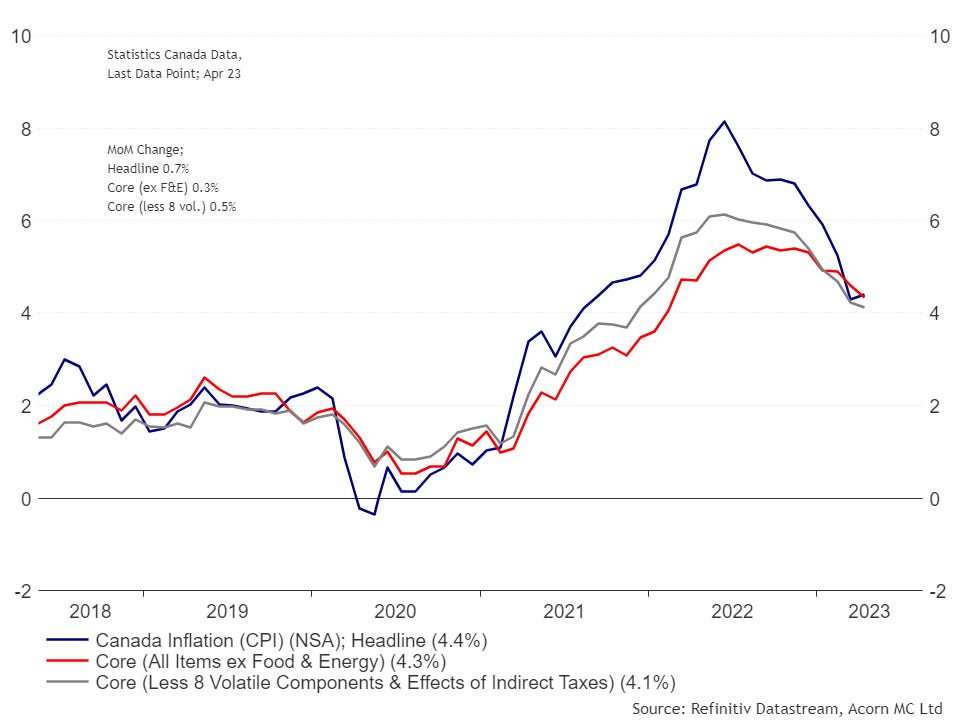

A couple of months after the Bank of Canada’s (BOC) victory lap and a declared pause in hikes, the Headline CPI rose year-on-year (YoY) to 4.4% from 4.3%, contrary to expectations of a decline. Moreover, month-on-month (MoM), headline rose by 0.7%, nearly doubling economists' expectations of 0.4%. As for Core CPI, which excludes volatile components, it only dropped to 4.1%, ending 6-months of steep decline.

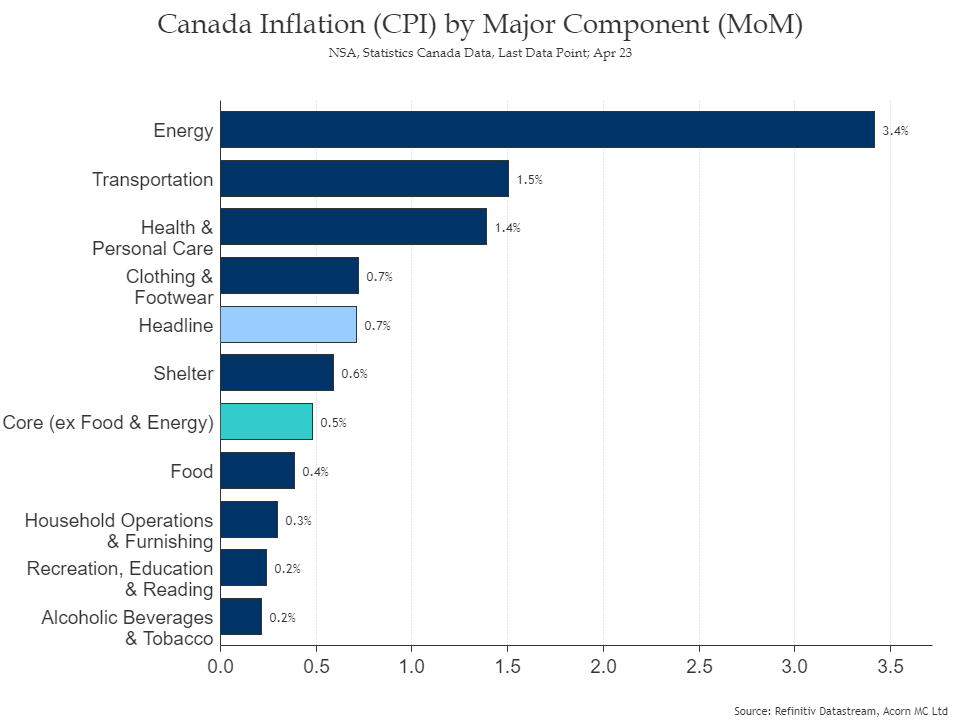

Each of the nine sub-components rose MoM. Energy and transportation jumped on the back of higher gasoline prices and carbon taxes. Food inflation MoM has finally slowed after a winter to forget. And Shelter’s contribution has begun to slow.

Energy, which constitutes approximately 7% of the Headline CPI basket, has been a significant drag on inflation. However, this situation might be reversing. Due to acute supply constraints and long-term constraints resulting from dogmatic green energy policies and insufficient refining capacity, energy prices may have reached their lower bound. It would necessitate a global recession to cut demand substantially and further reduce prices.

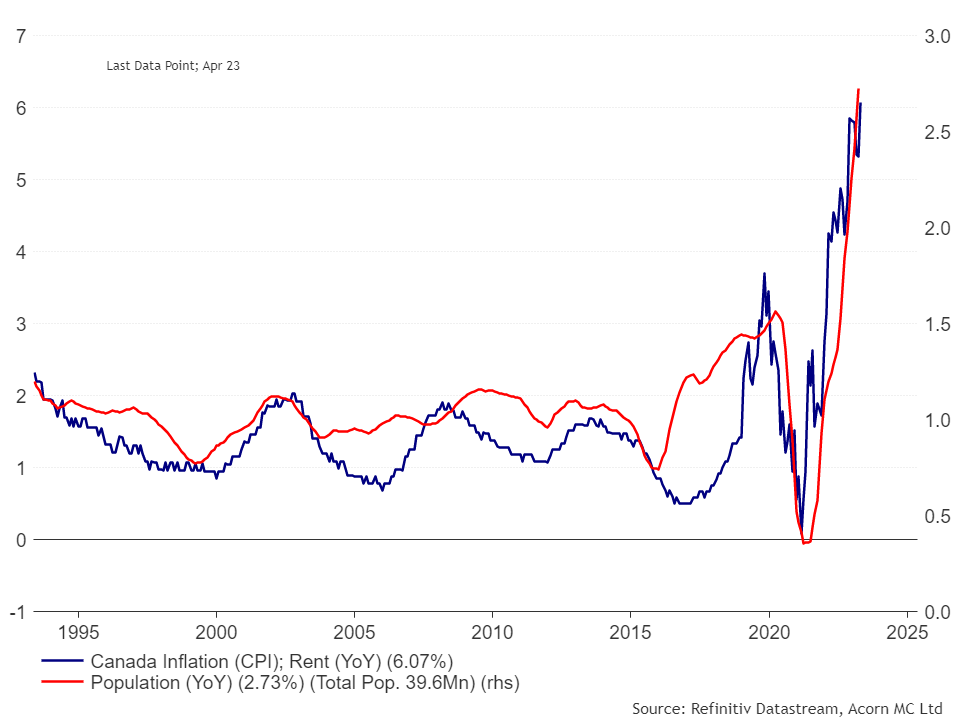

It is impossible to ignore the effect population growth is having on Canadian inflation -more bodies chasing after finite resources. Population growth, driven almost entirely by record immigration, has, without doubt, put upward pressure on the price of housing and put a floor under broader inflation too.

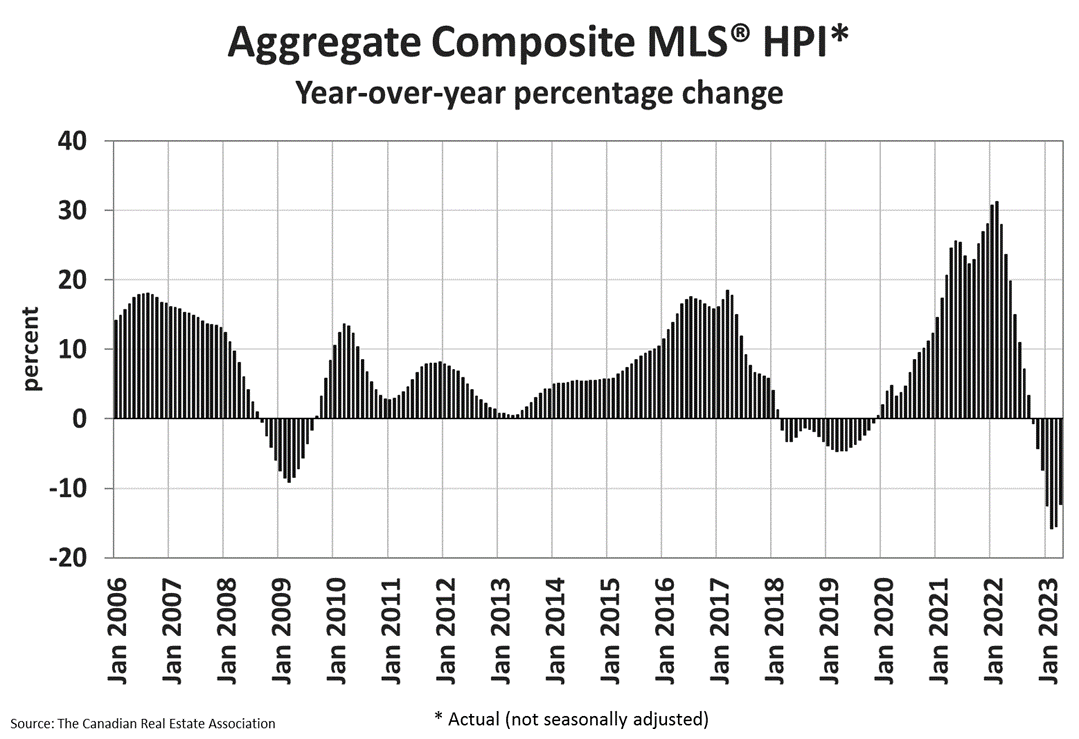

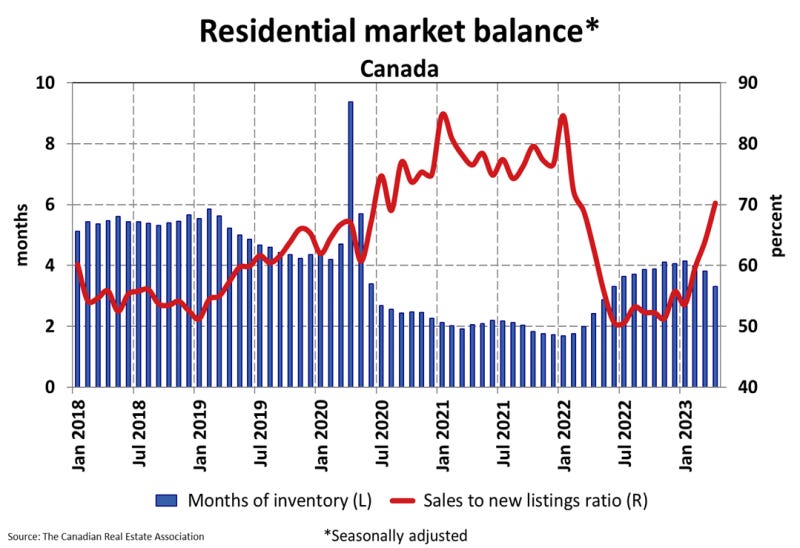

In Canada, house prices have stopped falling… for now. The MLS® Home Price Index (HPI) climb 1.6% month-over-month (MoM) but is down 12.3% year-over-year (YoY).

The number of newly listed homes rose 1.6% (MoM) in April, but New Supply is currently at a 20-year low and months of inventory fell back below 4, which is considered tight.

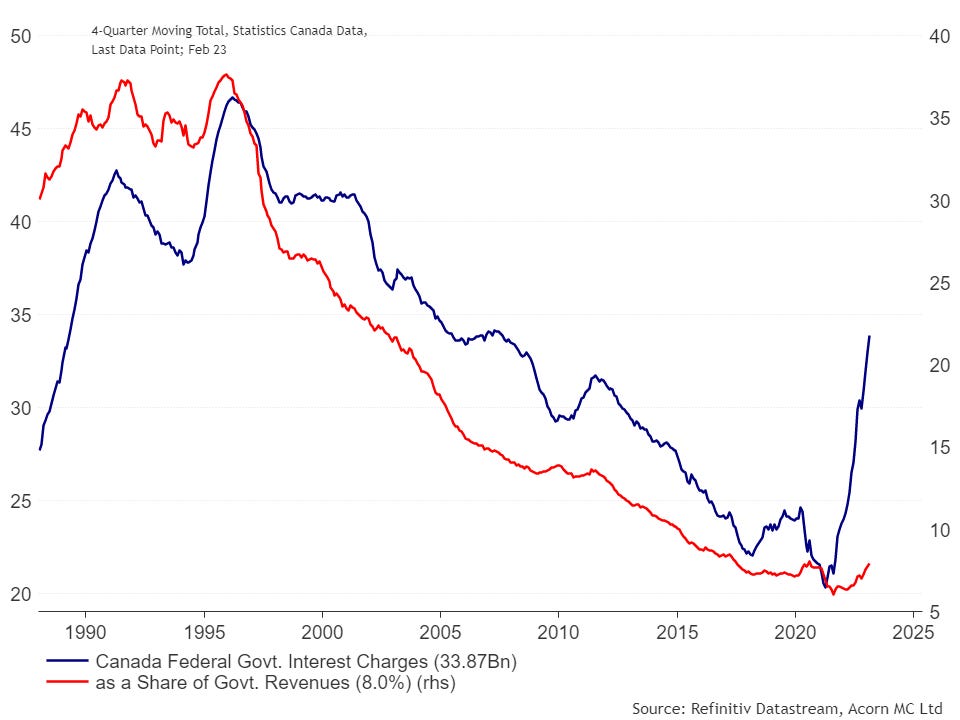

The Federal Government issued a lot of debt to pay for the pandemic spending spree. The problem is that nearly all the debt was issued at the front end of the yield curve (i.e., short-term). Fast-forward to today, the debt is maturing, and interest rates are much higher.

The maturing debt will have to be refinanced at much higher rates, and interest charges as a share of government revenue will jump, putting pressure on budgets over the near and long term.

Click below to listen to this week’s episode!